VA Loan Funding Fee Explained: Costs, Exemptions, and How It Works

Learn how the VA funding fee works, who is exempt, how much it costs, and how it affects your mortgage payment. Use our VA Mortgage Calculator to estimate costs.

Calcifyai Team

Expert calculators & financial tools

One of the most common questions homebuyers ask when exploring VA loans is: "What is the VA funding fee?"

While VA loans offer major benefits such as no down payment, no private mortgage insurance (PMI), and competitive interest rates, most borrowers are required to pay a one-time VA funding fee.

Understanding this fee is important because it directly affects your total loan amount and monthly mortgage payment.

In this guide, we'll explain what the VA funding fee is, why it exists, how much it costs, who is exempt, and how it impacts your mortgage.

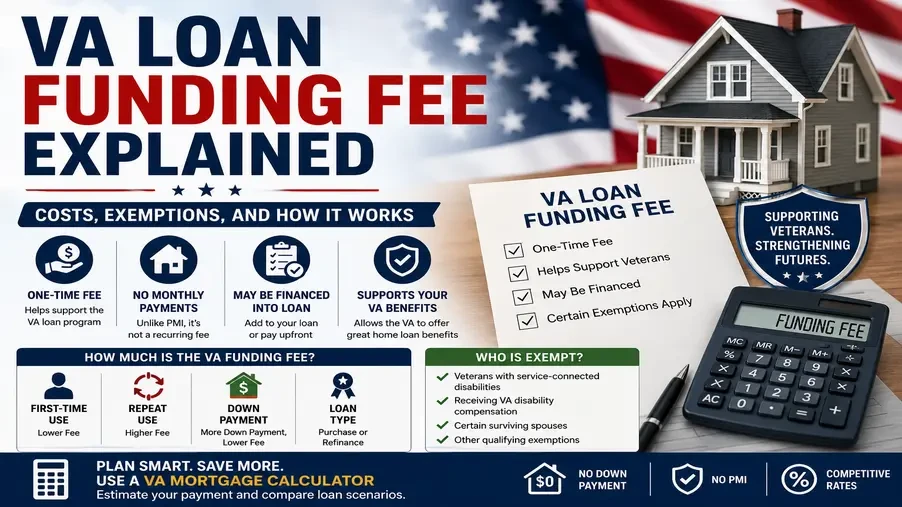

What Is the VA Funding Fee?

The VA funding fee is a one-time charge paid by most borrowers who use a VA home loan.

This fee helps support the VA loan program and reduces costs to taxpayers while allowing future veterans and military families to benefit from the program.

Unlike PMI on conventional loans, the funding fee is not a recurring monthly charge.

Instead, it is typically paid once at closing or added to the loan balance.

If you're new to the program, start by reading our guide on What Is a VA Loan? to understand how VA home loans work and why they remain one of the most affordable mortgage options available.

Why Does the VA Charge a Funding Fee?

The Department of Veterans Affairs guarantees a portion of every VA loan.

This guarantee reduces lender risk and allows borrowers to receive benefits such as:

No down payment

No PMI

Competitive mortgage rates

Flexible credit requirements

The funding fee helps offset the cost of providing these benefits.

Without the fee, the VA loan program would be significantly more expensive to operate.

How Much Is the VA Funding Fee?

The exact funding fee depends on several factors:

Factors That Affect the Fee

First-time or repeat use of a VA loan

Down payment amount

Type of VA loan

Military service category

Generally, borrowers who make larger down payments pay lower funding fees.

Likewise, first-time users often pay lower fees than repeat borrowers.

Example of a VA Funding Fee

Let's assume:

Home Purchase Price: $350,000

Down Payment: $0

First-Time VA Loan User

If the funding fee is financed into the loan:

Base Loan Amount = $350,000

Funding Fee Added = Included in Loan

Final Loan Balance = Higher than Purchase Price

This increases the amount financed and may slightly increase monthly mortgage payments.

Before applying, many borrowers use a VA Mortgage Calculator to estimate how financing the funding fee affects monthly payments and long-term interest costs.

Can You Finance the VA Funding Fee?

Yes.

Most borrowers choose to roll the funding fee into their mortgage instead of paying it upfront.

Option 1: Pay Upfront

Benefits:

Lower loan balance

Lower monthly payment

Less interest paid over time

Option 2: Finance the Fee

Benefits:

Lower upfront closing costs

Easier home purchase process

More cash available after closing

Both options are common and depend on your financial situation.

Who Is Exempt From the VA Funding Fee?

Some borrowers are not required to pay the funding fee.

Common exemptions include:

Veterans Receiving VA Disability Compensation

Borrowers receiving compensation for service-connected disabilities are generally exempt.

Eligible Surviving Spouses

Certain surviving spouses may qualify for funding fee exemptions.

Veterans Entitled to Disability Compensation

Some veterans awaiting compensation approval may also qualify.

Active-Duty Members With Qualifying Disability Determinations

Certain active-duty service members may receive exemptions based on disability status.

Because exemption rules can change, borrowers should verify their status with the VA or their lender.

Does Every VA Borrower Pay the Funding Fee?

No.

Many eligible veterans never pay the fee due to disability-related exemptions.

For everyone else, the funding fee is usually a required part of the mortgage process.

Your Certificate of Eligibility (COE) may indicate whether you're exempt.

To understand COE requirements, read our guide on VA Loan Eligibility Requirements.

Funding Fee vs PMI

Many homebuyers compare the VA funding fee to private mortgage insurance.

VA Funding Fee

One-time charge

May be financed

Supports the VA loan program

PMI

Monthly recurring cost

Common on conventional loans

Often required when down payment is below 20%

Although the VA funding fee can appear expensive initially, it is often significantly less costly than years of PMI payments.

How the Funding Fee Affects Monthly Payments

Because many borrowers finance the funding fee, it becomes part of the mortgage balance.

This can impact:

Monthly mortgage payment

Total interest paid

Long-term loan costs

The actual difference depends on:

Home price

Interest rate

Loan term

Funding fee amount

A VA Home Loan Calculator can help estimate these costs before applying.

Should You Pay the Funding Fee Upfront?

Paying the fee upfront may be beneficial if:

You have available cash reserves

You want lower monthly payments

You want to reduce total interest costs

Financing the fee may be beneficial if:

You want to minimize closing costs

You prefer keeping more cash available

You are purchasing with little upfront savings

There is no universal answer the best choice depends on your financial goals.

Common Funding Fee Myths

Myth #1: It's a Monthly Fee

False.

The VA funding fee is generally a one-time charge.

Myth #2: Everyone Pays It

False.

Many veterans qualify for exemptions.

Myth #3: You Must Pay It at Closing

False.

Most borrowers can finance the fee into their loan.

Myth #4: It Makes VA Loans Expensive

False.

Even with the funding fee, VA loans are often less expensive than conventional mortgages because they eliminate PMI and offer competitive rates.

Frequently Asked Questions

Can the VA funding fee be refunded?

In some situations, borrowers who later receive disability compensation may qualify for reimbursement.

Is the funding fee tax deductible?

Tax treatment varies and borrowers should consult a tax professional.

Can I avoid the funding fee?

Only eligible exempt borrowers can avoid the fee.

Does refinancing require a funding fee?

Some refinance programs may include funding fees, although rates often differ from purchase loans.

Is the funding fee included in monthly payments?

Not directly. However, if financed into the mortgage, it increases the loan balance and monthly payment.

Conclusion

The VA funding fee is a one-time cost that helps support one of the most valuable mortgage programs available to veterans and military families. While most borrowers pay the fee, many qualify for exemptions, and financing options make it easier to manage upfront costs.

Before choosing whether to pay the fee upfront or finance it into your loan, use our VA Mortgage Calculator to compare different scenarios and estimate your monthly payment.

Disclaimer

The information provided in this article is for educational and informational purposes only. It should not be considered as professional financial, medical, or legal advice. Always consult with qualified professionals for specific guidance related to your situation.

Popular Calculators

Explore our most-used free calculators for finance, health, and everyday needs.