Benefits of VA Home Loans: 10 Reasons Veterans Choose VA Financing

Discover the top benefits of VA home loans, including no down payment, no PMI, competitive rates, and flexible qualification requirements for eligible veterans.

Calcifyai Team

Expert calculators & financial tools

Buying a home is one of the largest financial commitments most people will ever make. For eligible veterans, active-duty service members, and military families, VA home loans offer a unique opportunity to achieve homeownership with fewer financial barriers.

Since their introduction in 1944, VA loans have helped millions of Americans purchase homes through favorable lending terms that are often unavailable with conventional mortgages.

From no down payment requirements to lower borrowing costs, VA loans provide significant advantages that can save borrowers thousands of dollars over the life of a mortgage.

In this guide, we'll explore the biggest benefits of VA home loans and explain why many military families choose VA financing over other mortgage options. And why choose our VA Mortgage Calculator to calculate your finance.

What Makes VA Loans Different?

VA loans are backed by the U.S. Department of Veterans Affairs and offered through approved lenders.

Unlike conventional mortgages, these loans are specifically designed to support military members and veterans.

If you're unfamiliar with how the program works, our beginner's guide to military-backed home financing explains the fundamentals of VA mortgages and how they differ from traditional home loans.

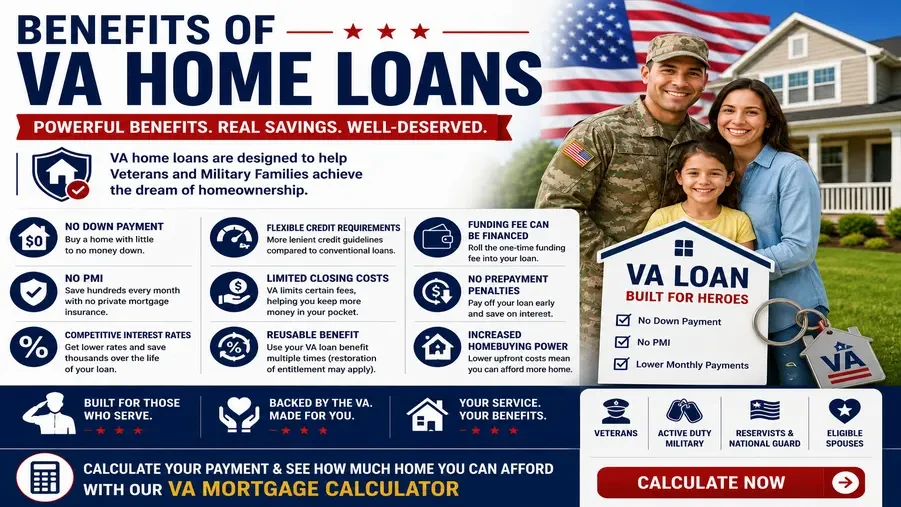

Benefit #1: No Down Payment Requirement

Perhaps the most well-known advantage of a VA loan is the ability to purchase a home with little or no money down.

Many traditional mortgage programs require buyers to save thousands—or even tens of thousands of dollars before purchasing a home.

VA financing can eliminate that obstacle.

Why This Matters

A lower upfront investment allows borrowers to:

Buy sooner

Keep emergency savings intact

Reduce financial stress

Avoid years of saving for a large down payment

For many first-time military homebuyers, this benefit alone makes homeownership possible.

Benefit #2: No Private Mortgage Insurance (PMI)

Most conventional mortgages require private mortgage insurance when the borrower puts less than 20% down.

PMI can add hundreds of dollars to a monthly mortgage payment.

VA loans eliminate this requirement.

Long-Term Savings

Without PMI, borrowers often enjoy:

Lower monthly payments

Improved affordability

Greater purchasing power

Over a 30-year mortgage, the savings can be substantial.

Benefit #3: Competitive Interest Rates

Because lenders receive protection through the VA guarantee, they often offer more favorable rates to qualified borrowers.

Lower rates can lead to:

Reduced monthly payments

Lower total interest costs

Greater long-term savings

Even a small difference in interest rates can significantly impact overall mortgage expenses.

If you're comparing financing scenarios, a military home affordability planner can help estimate how different rates affect your monthly budget.

Benefit #4: Flexible Credit Requirements

Many mortgage programs have strict credit score requirements.

VA loans tend to offer greater flexibility.

While lenders establish their own approval standards, VA financing often accommodates borrowers who may not qualify for the most competitive conventional loan programs.

This flexibility can benefit:

First-time buyers

Young military families

Borrowers rebuilding credit

For a deeper understanding of qualification standards, review our veteran home loan qualification guide before beginning the application process.

Benefit #5: Limited Closing Costs

Closing costs are an unavoidable part of buying a home, but VA loans include protections that help prevent excessive lender fees.

The Department of Veterans Affairs limits certain charges that lenders can pass on to borrowers.

This can reduce the amount of cash needed at closing and improve affordability.

Benefit #6: Funding Fee Can Be Financed

Most eligible borrowers pay a one-time funding fee when using a VA loan.

However, many choose to roll this cost into the mortgage rather than paying it upfront.

This allows borrowers to purchase a home with fewer out-of-pocket expenses.

If you're unsure how this fee works, our article covering upfront costs associated with VA-backed mortgages explains funding fees, exemptions, and financing options in detail.

Benefit #7: Reusable Loan Benefit

Many borrowers assume VA loan benefits can only be used once.

In reality, qualified borrowers may be able to use their entitlement multiple times throughout their lives.

This flexibility is particularly valuable for:

Military relocations

Career moves

Growing families

Home upgrades

Benefit #8: No Prepayment Penalties

VA borrowers can make extra mortgage payments or pay off their loan early without facing prepayment penalties.

Benefits include:

Faster loan payoff

Reduced interest costs

Increased equity growth

This provides additional flexibility for homeowners who want to eliminate debt sooner.

Benefit #9: Easier Refinancing Opportunities

VA borrowers often gain access to streamlined refinance programs designed to reduce paperwork and simplify the refinancing process.

Benefits may include:

Lower interest rates

Reduced monthly payments

Simplified approval procedures

These options can help homeowners save money when market rates decline.

Benefit #10: Increased Homebuying Power

When borrowers avoid PMI and large down payments, they often have more purchasing power.

This means they may be able to:

Purchase a larger home

Buy in a preferred neighborhood

Maintain stronger cash reserves

Handle unexpected expenses more comfortably

Using a monthly housing cost estimator for veterans can help determine how much home fits within your budget before starting your home search.

VA Loans vs Conventional Mortgages

Many military borrowers compare VA loans with conventional financing.

In many cases, VA loans provide:

Lower upfront costs

Lower monthly payments

Greater qualification flexibility

Reduced mortgage insurance expenses

If you're still evaluating both options, our comparison of government-backed military mortgages versus traditional home financing provides a detailed breakdown of costs and benefits.

Frequently Asked Questions

Are VA loans only for first-time homebuyers?

No. Eligible borrowers can often use their benefits multiple times.

Do VA loans require perfect credit?

No. VA financing generally offers more flexibility than many conventional loan programs.

Is a down payment always required?

Many eligible borrowers purchase homes with no down payment.

Can VA loans save money?

Yes. Lower rates, no PMI, and reduced upfront costs can produce significant savings.

Are VA loans worth it?

For many eligible veterans and military families, VA loans are among the most affordable mortgage options available.

Conclusion

VA home loans provide valuable advantages that can make homeownership more accessible and affordable for eligible military borrowers. From no down payment requirements to competitive interest rates and no PMI, these benefits often result in substantial savings compared with traditional financing options.

Before starting your home search, consider using a mortgage budgeting tool built for military borrowers to estimate monthly payments and compare financing scenarios.

Disclaimer

The information provided in this article is for educational and informational purposes only. It should not be considered as professional financial, medical, or legal advice. Always consult with qualified professionals for specific guidance related to your situation.

Popular Calculators

Explore our most-used free calculators for finance, health, and everyday needs.