How Much House Can You Afford with a VA Loan? Complete Affordability Guide

Learn how much house you can afford with a VA loan. Understand income requirements, DTI ratios, interest rates, and affordability factors before buying a home.

Calcifyai Team

Expert calculators & financial tools

One of the first questions homebuyers ask before beginning their property search is:

"How much house can I actually afford?"

For veterans, active-duty military members, and eligible military families, VA loans often increase buying power compared to traditional mortgage options.

Because VA financing typically requires no down payment and no private mortgage insurance (PMI), many borrowers discover they can comfortably afford more home than they initially expected.

However, affordability isn't determined solely by lender approval. A mortgage that fits comfortably within your budget today should remain manageable for years to come.

In this guide, we'll explore the factors that determine VA loan affordability and show you how to estimate a realistic homebuying budget.

Understanding Home Affordability

Affordability refers to the amount of home you can purchase while maintaining healthy finances.

Many borrowers focus only on the maximum loan amount a lender will approve.

A smarter approach is evaluating:

Monthly mortgage payment

Property taxes

Homeowners insurance

Utility costs

Maintenance expenses

Existing debt obligations

Future financial goals

The goal isn't simply buying the most expensive home possible, it's purchasing a home you can comfortably afford.

Why VA Loans Increase Buying Power

VA financing offers several advantages that can improve affordability.

No Down Payment Requirement

Many conventional mortgages require a significant upfront investment.

With eligible VA financing, borrowers can often purchase a home without spending years saving for a down payment.

This allows military families to preserve cash reserves for:

Emergencies

Moving expenses

Home improvements

Future investments

No Monthly PMI Costs

Private mortgage insurance can add hundreds of dollars to monthly housing expenses.

Because VA loans generally eliminate PMI, borrowers often have more room in their budget for housing costs.

This advantage alone can significantly increase purchasing power.

If you're evaluating the financial advantages of military-backed financing, explore our article covering the largest advantages available through VA home loans.

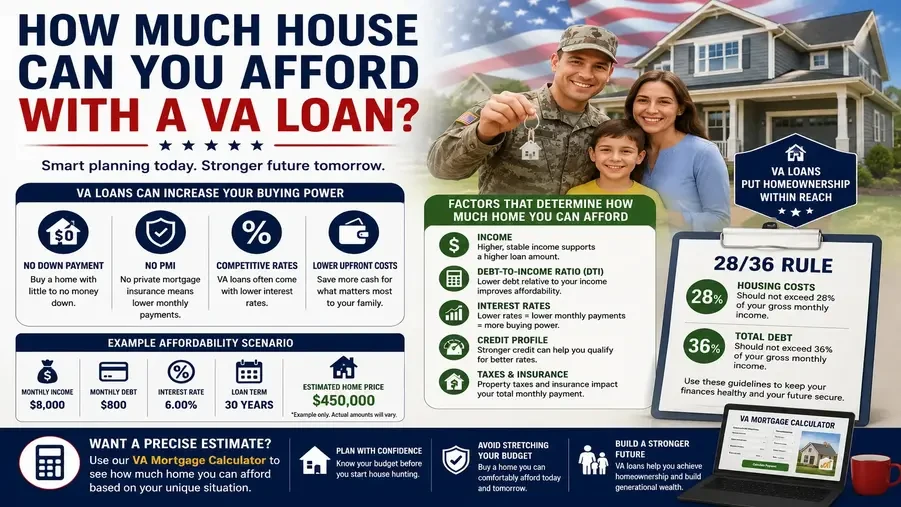

Factors That Determine How Much Home You Can Afford

Several factors influence your homebuying budget.

Income

Your household income is one of the most important affordability factors.

Lenders evaluate:

Base salary

Military allowances

Bonus income

Self-employment income

Other qualifying earnings

Generally, higher income supports a larger mortgage.

Debt-to-Income Ratio (DTI)

Lenders compare your monthly debt obligations to your gross monthly income.

Common debts include:

Auto loans

Credit cards

Student loans

Personal loans

Lower debt levels generally improve affordability.

Credit Profile

Although VA loans offer flexibility, stronger credit profiles often result in:

Better mortgage rates

Lower monthly payments

Greater purchasing power

Borrowers interested in lender qualification standards should review our military borrower approval requirements guide before applying.

Interest Rates

Mortgage rates have a direct impact on affordability.

For example:

Lower rates = lower monthly payments

Higher rates = reduced buying power

Even a small rate difference can change how much home you qualify for.

Property Taxes and Insurance

Two homes with identical prices can have very different monthly payments depending on:

Local property tax rates

Homeowners insurance costs

Flood insurance requirements

These expenses should always be included when calculating affordability.

The 28/36 Rule

Many financial experts recommend the 28/36 guideline.

Housing Costs

No more than 28% of gross monthly income should go toward housing expenses.

Total Debt

No more than 36% of gross monthly income should go toward total debt obligations.

While VA lenders often allow flexibility, these benchmarks provide a useful starting point.

Example VA Loan Affordability Scenario

Let's assume:

Household Income

$8,000 per month

Monthly Debt

$800 per month

Estimated Interest Rate

6%

Loan Term

30 Years

Under these circumstances, a borrower may qualify for substantially more purchasing power than someone using conventional financing due to the absence of PMI and lower upfront requirements.

The exact amount varies by lender and financial profile.

Estimate Your Budget Before House Hunting

Many homebuyers make the mistake of shopping for homes before understanding their true budget.

A better strategy is using a home financing estimator designed for veterans to calculate:

Monthly mortgage payments

Taxes and insurance

Interest expenses

Total housing costs

This provides a realistic budget before contacting lenders or real estate agents.

Why Lender Approval Doesn't Equal Affordability

Just because a lender approves a certain loan amount doesn't mean it's the right choice.

Before selecting a home, consider:

Retirement savings goals

Emergency funds

Future family expenses

Travel plans

Lifestyle preferences

Many borrowers intentionally choose homes below their maximum approval amount to maintain financial flexibility.

Common Affordability Mistakes

Buying Based Only on Approval Amount

Approval limits should be considered a ceiling, not a target.

Ignoring Future Expenses

Life circumstances change.

Consider future costs before stretching your budget.

Forgetting Maintenance Costs

Homeownership includes expenses beyond the mortgage payment.

Not Comparing Loan Scenarios

Different rates, terms, and property taxes can significantly affect affordability.

How VA Loans Compare to Conventional Mortgages

Military borrowers often discover they can afford more home through VA financing because of:

No PMI

Lower upfront costs

Competitive rates

Flexible qualification standards

If you're still comparing mortgage options, our breakdown of government-backed military loans versus traditional mortgage programs explains the differences in greater detail.

Frequently Asked Questions

How much house can I afford with a VA loan?

The answer depends on income, debt, interest rates, taxes, insurance, and lender requirements.

Do VA loans increase buying power?

In many cases, yes. The absence of PMI and down payment requirements can improve affordability.

Is there a maximum home price for VA loans?

Many borrowers with full entitlement have no official VA loan limit, although lender qualification standards still apply.

Can I buy a home with no down payment?

Many eligible borrowers can purchase homes without a down payment using VA financing.

Should I borrow the maximum amount available?

Not necessarily. Choosing a comfortable payment is often the better long-term financial decision.

Conclusion

VA loans provide eligible military borrowers with one of the most affordable paths to homeownership. Benefits such as no down payment requirements, no PMI, and competitive mortgage rates often increase purchasing power and make homeownership more accessible.

Before beginning your home search, use a VA-specific mortgage budgeting calculator to estimate monthly payments and determine a comfortable home price range.

Disclaimer

The information provided in this article is for educational and informational purposes only. It should not be considered as professional financial, medical, or legal advice. Always consult with qualified professionals for specific guidance related to your situation.

Popular Calculators

Explore our most-used free calculators for finance, health, and everyday needs.