Mortgage Overpayment Calculator Guide: How Overpaying Your Mortgage Can Save Thousands

Learn how mortgage overpayments work, how much interest you can save, and how to pay off your mortgage years earlier using smart overpayment strategies.

Calcifyai Team

Expert calculators & financial tools

For many homeowners, a mortgage is the largest debt they'll ever have. While monthly payments may seem fixed, many lenders allow borrowers to make additional payments toward their mortgage balance.

These extra payments are known as mortgage overpayments.

Even small overpayments can reduce the total interest paid, shorten the mortgage term, and help you become mortgage-free sooner.

Whether you're looking to save money, reduce financial stress, or build equity faster, understanding mortgage overpayments can be a valuable part of your financial strategy.

A UK Mortgage Calculator can help you estimate how much time and interest you could save through regular overpayments.

What Is a Mortgage Overpayment?

A mortgage overpayment is any payment you make above your required monthly mortgage payment.

For example:

Required Monthly Payment = £1,200

Actual Payment = £1,300

Monthly Overpayment = £100

The additional £100 goes directly toward reducing your mortgage balance.

Because interest is calculated on the remaining balance, reducing that balance earlier often results in substantial long-term savings.

How Mortgage Overpayments Work

Every mortgage payment consists of:

Principal repayment

Interest charges

When you make an overpayment, more money goes toward reducing the principal balance.

As the outstanding balance decreases:

Future interest charges decrease

Mortgage term shortens

Total borrowing cost falls

This creates a compounding benefit over time.

Why Consider Mortgage Overpayments?

Many homeowners focus solely on making their required payments.

However, overpaying can provide several financial advantages.

Pay Off Your Mortgage Faster

One of the biggest benefits is reducing the length of your mortgage.

For example:

A 25-year mortgage could potentially be reduced by several years through consistent overpayments.

Save Thousands in Interest

Interest accumulates over decades.

Reducing the balance early means less interest is charged throughout the life of the loan.

Build Home Equity Faster

Overpayments increase your ownership stake in the property.

This may improve future remortgaging opportunities.

Improve Financial Security

Becoming mortgage-free sooner can provide greater financial flexibility and peace of mind.

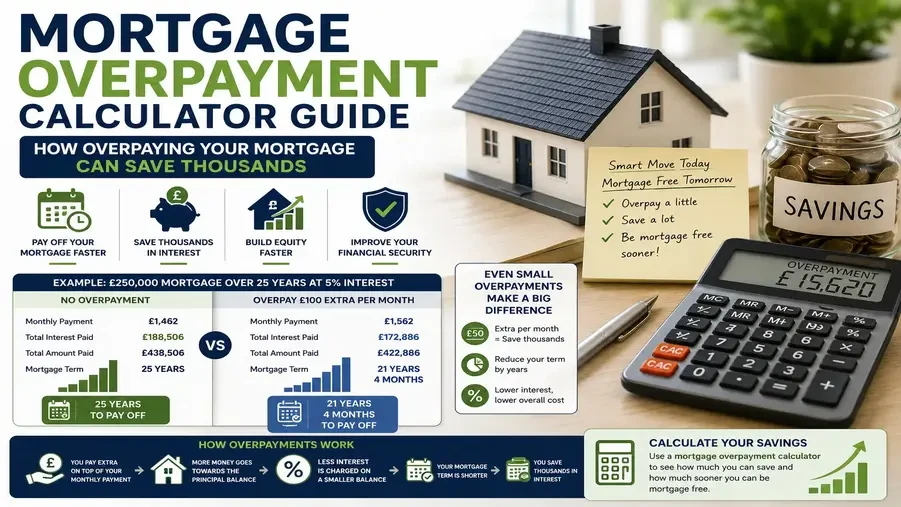

Example of Mortgage Overpayment Savings

Let's assume:

Mortgage Balance: £250,000

Interest Rate: 5%

Term: 25 Years

Monthly Payment: £1,462

Now add an extra £100 monthly overpayment.

Potential Results

Scenario | Standard Mortgage | With £100 Overpayment |

Monthly Payment | £1,462 | £1,562 |

Mortgage Term | 25 Years | Approximately 21–22 Years |

Interest Paid | Higher | Significantly Lower |

While exact savings vary, many homeowners save tens of thousands of pounds through consistent overpayments.

A mortgage savings estimator can help calculate your specific savings.

Regular vs Lump Sum Overpayments

There are generally two ways to overpay a mortgage.

Regular Monthly Overpayments

Adding a fixed amount to each monthly payment.

Example:

£50 extra per month

£100 extra per month

£200 extra per month

This approach is popular because it's predictable and easy to budget.

Lump Sum Overpayments

Making occasional larger payments.

Examples include:

Annual work bonus

Tax refund

Inheritance

Investment gains

Even a single lump sum payment can significantly reduce future interest costs.

How Much Should You Overpay?

There is no universal answer.

The best amount depends on:

Income

Savings goals

Emergency fund

Other debts

Investment opportunities

Many financial advisers recommend balancing mortgage overpayments with:

Retirement contributions

Emergency savings

Debt repayment

Investment goals

A home loan repayment planner can help model different scenarios before committing to an overpayment strategy.

Check Your Mortgage Overpayment Limits

Many mortgage lenders allow overpayments, but restrictions often apply.

Typical limits include:

Up to 10% of outstanding balance per year

Fixed annual overpayment allowance

Early repayment charge thresholds

Exceeding these limits may trigger fees.

Always review your mortgage agreement before making large overpayments.

When Mortgage Overpayments Make Sense

Mortgage overpayments may be beneficial if:

You Have High Mortgage Interest Rates

The higher your rate, the greater the potential savings.

You Have Emergency Savings

Ensure you maintain an emergency fund before making significant overpayments.

You Want to Become Mortgage-Free Earlier

Overpayments can dramatically shorten mortgage terms.

You Prefer Guaranteed Returns

Paying down debt provides a predictable financial benefit.

When Mortgage Overpayments May Not Be the Best Choice

Overpaying isn't always the optimal financial decision.

Consider alternatives if:

You Have High-Interest Consumer Debt

Credit cards often carry much higher interest rates than mortgages.

You Lack Emergency Savings

Liquidity is important for unexpected expenses.

Your Employer Offers Retirement Matching

Some retirement contributions may provide greater long-term value.

You Have Better Investment Opportunities

Depending on market conditions, investments may potentially generate higher returns.

Mortgage Overpayments vs Remortgaging

Some homeowners wonder whether they should overpay or remortgage.

Mortgage Overpayments

Reduce balance faster

Save interest

Shorten term

Remortgaging

Potentially secure lower interest rates

Change loan terms

Access home equity

Many homeowners use both strategies together.

You can learn more in our guide on Remortgaging Explained.

Common Mortgage Overpayment Mistakes

Overpaying Without Emergency Savings

Always maintain financial reserves.

Ignoring Early Repayment Charges

Check lender restrictions before making large payments.

Neglecting Other Financial Goals

Balance mortgage reduction with investing and retirement planning.

Not Calculating Potential Savings

Use a loan overpayment calculator to estimate benefits before committing additional funds.

How a Mortgage Overpayment Calculator Helps

A mortgage overpayment calculator allows homeowners to:

Estimate interest savings

Compare overpayment amounts

Calculate mortgage term reduction

Model lump-sum payments

Evaluate repayment strategies

Using a mortgage term reduction calculator can provide a clear picture of how extra payments impact your mortgage timeline.

Frequently Asked Questions

Can I overpay my mortgage every month?

Yes. Most lenders allow regular overpayments, although limits may apply.

Do mortgage overpayments reduce monthly payments?

Usually, overpayments reduce the mortgage balance and term rather than monthly payments.

Are mortgage overpayments worth it?

For many homeowners, yes. Overpayments can significantly reduce interest costs and shorten the mortgage term.

Can I make a lump sum mortgage payment?

Many lenders allow lump-sum payments, but check for overpayment limits or early repayment charges.

How much interest can I save?

Savings vary depending on mortgage balance, rate, term, and overpayment amount.

Final Thoughts

Mortgage overpayments can be one of the most effective ways to reduce borrowing costs and become mortgage-free sooner.

Even relatively small extra payments can save thousands of pounds in interest and shorten your mortgage by several years.

Before making overpayments, review your lender's rules, assess your overall financial situation, and calculate potential savings. With the right strategy, mortgage overpayments can become a powerful tool for long-term financial freedom.

Disclaimer

The information provided in this article is for educational and informational purposes only. It should not be considered as professional financial, medical, or legal advice. Always consult with qualified professionals for specific guidance related to your situation.

Popular Calculators

Explore our most-used free calculators for finance, health, and everyday needs.